Chapter 11 - Dealing With Investment Mistakes

Nobody likes to make mistakes, but reality is that mistakes do happen from time to time, and are guaranteed to occur in the world of investing. So the question is not whether you will make mistakes, but rather how you will deal with mistakes. A lot of the discussion in this chapter is probably not unique to investing, but certainly more important to the world of investing, where the basis of most transactions is rooted in client trust. It takes a long time to build trust, but just a moment to lose it. Since I spent a lot of time discussing my investment process and how or why it was successful earlier in the book, I thought it necessary to add this chapter about investment mistakes, so that I could come clean about at least a couple of mistakes I know I have made.

Does your favorite mutual fund or hedge fund make investment mistakes? Are those mistakes and their resolution communicated to you? If you are paying a management fee for someone to manage your investments, shouldn’t they provide sufficient transparency for you to know how your investment manager is making investment decisions? Does reading a quarterly or yearly newsletter satisfy all your curiosities about how your assets are being managed? How does your investment manager determine she has made a mistake? What’s your investment manager’s process for rectifying mistakes?

I recently asked a well-known portfolio manager at a well-reputed mutual fund that prides itself in its fundamental analysis-driven investing process, what his process was to determine whether he had made a mistake with a particular stock. His answer – “the market tells us that we made a mistake”. Do you think that answer is consistent with his stated strategy of fundamental analysis, based on everything we discussed in this book so far? Unless he is holding a stock for a short-term trade, a fundamentals-driven manager should not be looking to the market to tell him whether he picked the right stock. For a fundamentals-driven manager, determination of a stock selection error would occur only upon learning that he made a mistake in analyzing underlying business fundamentals, which he should be tracking carefully. At least he was honest, or perhaps he didn’t have a chance to think about his answer. Either way, his response is certainly not unique, and a number of honest and well-known portfolio managers will probably answer the same way. Perhaps this serves to highlight the tension that such managers live with every day – to advertise to their clients that the fund is fundamentals-driven, but accept the reality that fund managers look to the market for answers far too often than they should.

In this chapter I am going to discuss a couple of the mistakes I have made in my investment analyses over the years, and what I have learnt from them.

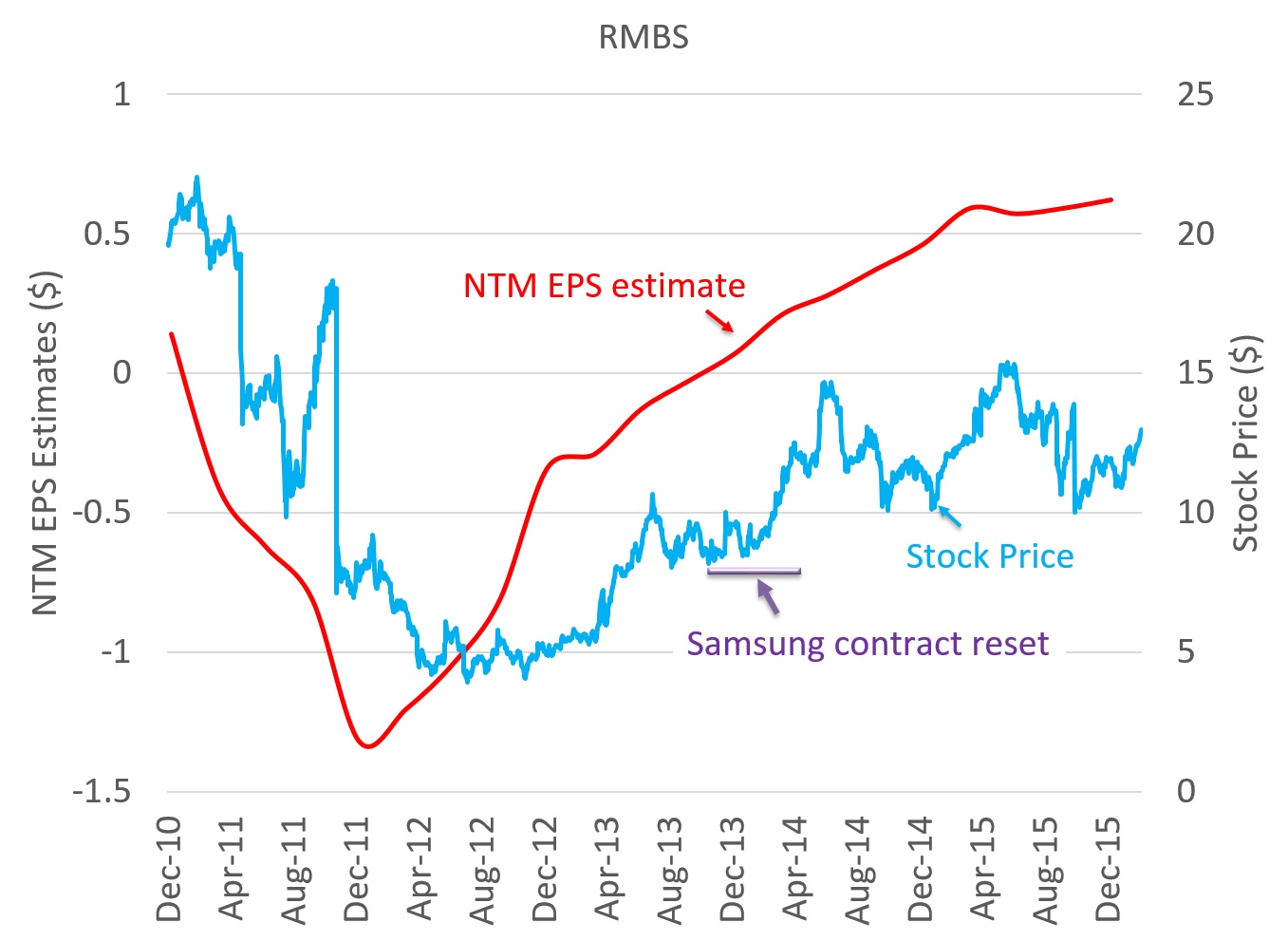

RMBS case study – Samsung contract reset

I initiated coverage of RMBS in December 2013 with a Buy rating because I was convinced that a positive inflection in Samsung’s DRAM revenues would translate into commensurately positive inflection in Rambus’ DRAM-related royalties from Samsung. After having analyzed the DRAM industry in detail, and estimating a high correlation between Samsung’s DRAM revenues and Rambus’ DRAM-related royalties from Samsung, I was confident that significant earnings upside was likely for RMBS. In early-January 2014, just a few weeks after my initiation of coverage, Rambus announced that Samsung had reset its contract with Rambus to a lower rate of royalties. With my primary investment thesis on the stock having proven wrong by an unexpected contract reset, I downgraded the stock to a Hold rating on the news.

The problem here was the binary nature of the fundamentals driving the Buy recommendation. Even though there was nothing wrong with my analysis, there wasn’t enough of a margin of safety in the Buy recommendation, given that it was singularly driven by DRAM upside, assuming Samsung would continue to pay royalties at the existing rate. The Rambus case study underscored the need to have a multi-factor investment thesis, such that if one of the factors didn’t play out as expected, you could still hold on to the stock for other reasons. That unfortunately was not the framework I had used for Rambus.

The next case study illustrates that even after having a multi-factor investment thesis, it is possible to be wrong on a stock, again due to no specific fault of your own except perhaps that you didn’t anticipate the level of expectations already baked into the stock before deciding to buy it.

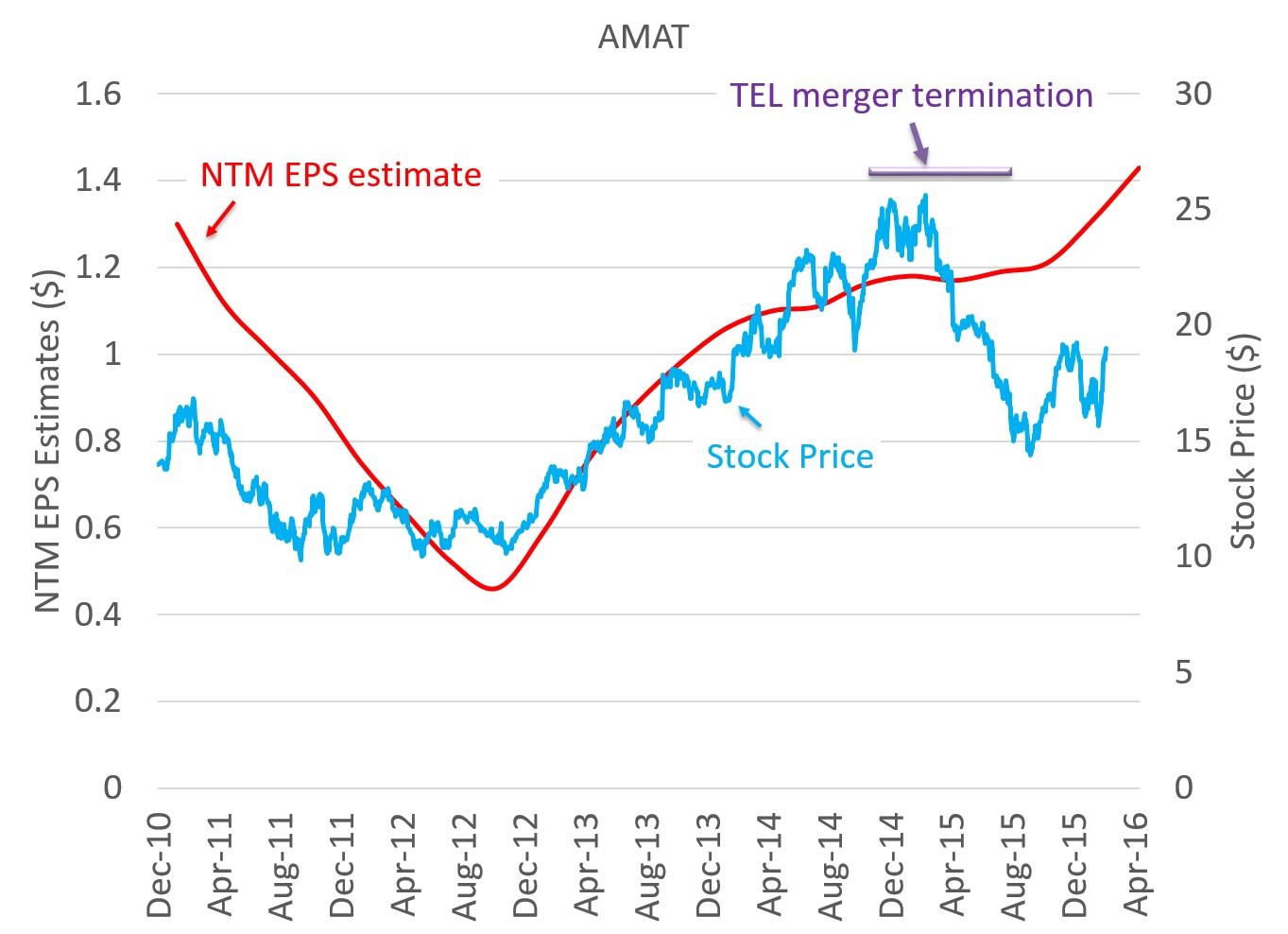

AMAT case study – TEL merger termination

I recommended Applied Materials (NASDAQ: AMAT) with a Buy rating starting in early-2014, based on a multi-factor secular thesis, which included a positive inflection due to AMAT’s planned merger with Tokyo Electron (TEL). Following several delays, AMAT finally announced in early 2015 that it had terminated its merger agreement with TEL due to regulatory hurdles in closing the merger. Following announcement of termination of its TEL merger, AMAT stock took a big hit, from the mid-$20s to the mid-$teens. The mistake I made here was not accounting for a sufficient margin of safety with my Buy recommendation.

If you look at the red line (NTM EPS estimate) in the chart above, you can interpret that standalone fundamentals for AMAT had performed solidly as of this writing, and this suggests that non-merger-related positive secular factors included in my Buy thesis played out more or less as expected. Not properly assessing how much merger-related euphoria was already baked into the stock price, was the mistake here. Since early-2014, AMAT had consistently traded at a NTM P/E multiple of ~18x, i.e. roughly in line with its peer group. In other words, AMAT was not trading at a significant valuation discount, and had not significantly underperformed in the period leading to my Buy recommendation. If you compare these factors to the framework I presented in Chapter 6, you will find that the margin of safety considerations were not satisfactorily met. Treating the TEL-merger as a high-probability scenario was the culprit.

As it turns out, as of this writing, secular fundamentals for AMAT I thought were still positive, virtually for the same reasons that they were positive in early 2014 (ex-TEL). With the stock having underperformed due to the TEL-merger debacle, the stock carried a higher margin of safety trading in the mid-$teens, though the stock’s valuation multiple remained healthy.

Why Value Investing in Technology is Difficult for Generalists

The chart below is a modified version of a chart you saw in Chapter 3 where we discussed what drives stock prices. This chart dissects “Company Fundamentals” into “Business Model” and “Industry Dynamics”. While a generalist value investor would be capable of understanding the business model of a technology company, she may not fully understand the influence that various industry dynamics might have on the company’s business model. This affects the process of assessing intrinsic value, and introduces risk in the investment process, making the process difficult to execute successfully.

As I have said throughout this book, if you are investing in technology stocks, but don’t think you have a strong understanding of underlying technology industry dynamics, then I’m afraid you might be misleading yourself or your investors. Furthermore, your chosen investment strategy is then most definitely not “fundamentals-driven”, but rather driven by some other short-term oriented trading strategy that may or may not have a popular name – like “technical trading” or “swing trading” or “momentum trading”.

Next in Chapter 12, I provide a framework to think about different types of information and data that are available to a technology investor, and discuss my best practices for using such information.